Table of Contents

In our previous blog post we started to explain why we started Hack Coworking: to solve issues the industry is facing in order to create the better future of coworking in a collaborative way, driven by members of coworking spaces. But the thing is, when we started Hack Coworking back in 2019, COVID-19 was not on the map. As building the future of coworking means understanding its present, we needed to address, during Hack Coworking Online, the true impact COVID-19 had on the coworking industry globally.

Tough challenge you might think. Well, not really when you know coworkintel, the global measurement and data analytics company that provides trusted intelligence services to the Coworking Industry. We invited Ben Tannenbaum, CEO of Coworkintel, to present the extensive global online survey they ran from March 2020 to May 2020 across 300 coworking spaces to concretely measure the impact of COVID-19 on the coworking industry.

Below, the takeaways of his talk.

A survey focused on the impact on occupancy, employee count as well as their predictions for the future.

The first thing that Ben pointed out in his talk is the fact that, on average, and based on the data they collected, the industry coped fairly well with the pandemic although, for a certain part of the respondents, the pandemic had dramatic consequences on their businesses.

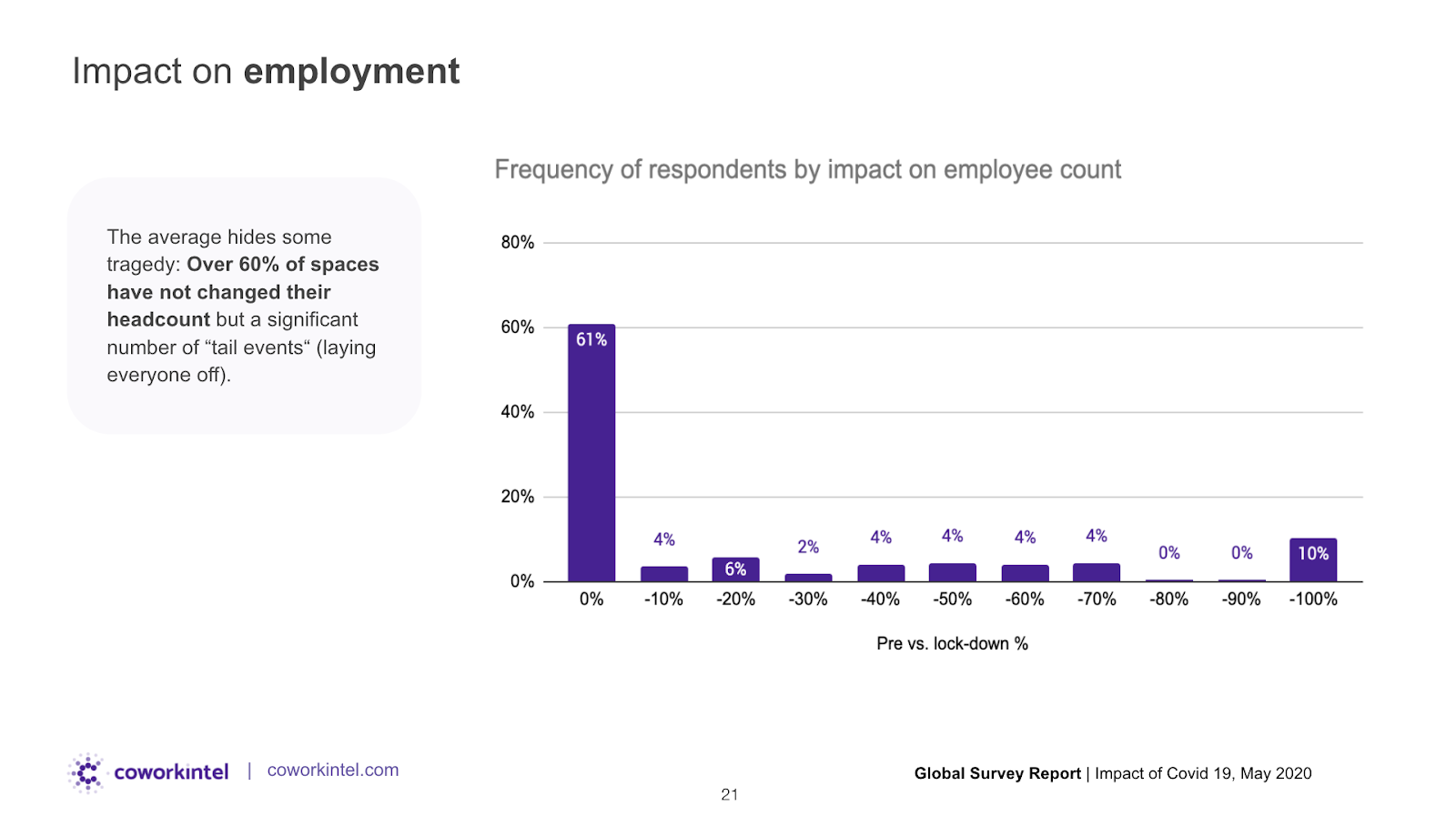

“As an example and on average, the employee count drop is around 16% but 10% of the respondents lost their entire employee count.”

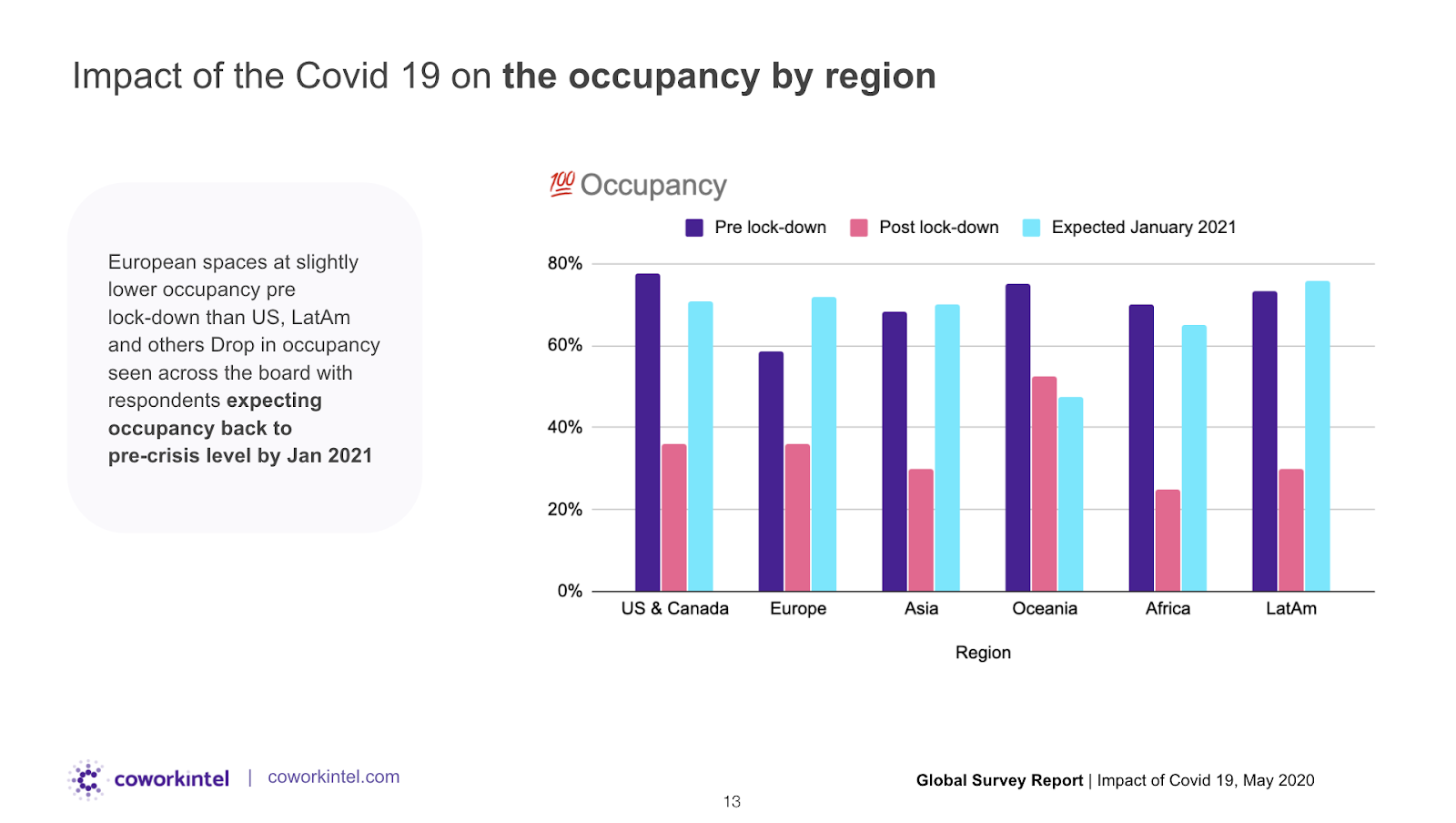

Looking at the survey highlights, which Ben covered in detail later on in his talk, the industry, noticed a 57% drop in occupancy

Another interesting data here is the expected recovery date. Respondents estimated that it will take at least 6 months to recover and get back to the occupancy level they had prior to the pandemic.

“The people who answered the survey were relatively young spaces” said Ben. Looking at the data, you can see that 70% of them have been open for about 2 years and, with no big surprises, that most of the spaces are under leasing contracts. What’s interesting here is that it shows that 2018 has been a pivotal year for the coworking industry with many new openings globally.

In 2 years of opening, respondents were able to reach, on average, around 57% occupancy, a fairly good number that dropped, as we learned through coworkintel results to 43% during the lockdown. Looking deeper into occupancy, it is interesting to notice that prior to the lockdown, occupancy level was lower in Europe than across other continents. That being said, the decrease of occupancy has been quite similar across the world, with a post lockdown looking quite promising globally.

Zooming in Europe, the country that has seen the highest drop in occupancy was the UK (-64%). In comparison, Germany saw a lower drop (-10%), which can be explained by the fact that the lockdown policies in Germany have been less severe than in the rest of Europe.

“According to the data, it takes 4 to 5 years for spaces to reach around 80% of occupancy”

Analyzing the survey outcome and putting in perspective the year of opening of spaces who responded to the survey, it is interesting to notice that on average and globally, it takes around 4 to 5 years to reach a steady 80% occupancy level. Ben explained that the first 4 years are really a way for spaces to create brand awareness as well as fine-tune their business model, leading later on to stable monthly revenues.

“Larger spaces had larger retention rates”

A data that can be explained by the fact that larger spaces have stronger cancellation policies but also by the fact that larger companies, who occupy those types of spaces, had the financial resources to keep their memberships throughout the lockdown.

“There is a fair split between spaces who renegotiated their leases and those who didn’t”

Out of all the respondents, 70% of them are leasing their coworking spaces. Among those 70%, 47.4% of them renegotiated their leasing contracts with their landlords during the lockdown period. Diving deeper into the topic and looking at it by regions and countries, we can see that the UK did not a very large portion of spaces who were able to renegotiate their leases (25% of them only) compared to Germany or even Latam who had above 80% of respondents renegotiating their terms.

“61% of responding spaces didn’t have any changes in their team but 10% of them had to let go everyone”

Globally, it seems like spaces were able to keep their teams together throughout the lockdown thanks to financial help that has been made available in different countries as well as other measures like reducing the number of hours worked during the time their spaces were not accessible. That being said, for 10% of the spaces who took the survey, the results look very different as they had to let go of all their employees. Looking at the data post COVID-19, it seems like regions like Europe, Asia and Latam expect to hire quickly upon reopening. Interestingly enough, teams that have been mostly impacted when it comes to reducing their sizes are teams from larger spaces, managing anywhere from 1,000 to 4,000 sqm.

“Operators felt that their landlords were more supportive than their governments”

A third of the respondents estimated that their governments supported their businesses in any way as opposed to half of the respondents who believed their landlords were quite supportive throughout the lockdown.

Looking at the future and as a wrap up of his talk, Ben highlighted that half of the spaces who took the survey believe the pandemic was a temporary setback and the industry will grow stronger upon reopening while ⅔ of the respondents estimated that their operations will look very different once they are able to reopen. A data that can be explained by the fact that most spaces will have to reinforce their safety and health measures to provide a safe place for everyone to return to. In terms of expected changes, operators also expect higher demands in private offices and lower demand in flex desks, a number that can be explained by the fact that members want to have a space of their own rather than not knowing who was there before.

Opening up the event with fresh data sets has been a great way for the audience to later on put things in perspective for the future. All and all, Ben highlighted that the industry remains relatively optimistic about its future, with many spaces expected more demands from larger companies. If you are curious to keep diving into the future of coworking, bookmark this blog into your favorite and keep a close eye for our next article on “Workplace Adaptation: 2020 and beyond” by Sombat Ngamchalermsak, Co-Founder & Director at Paperspace in Bangkok. Lastly, if you are interested to access Ben’s presentation, you can do so by clicking here.